Navigating health insurance can often feel overwhelming due to the numerous technical terms used. If you’re new to health insurance or just trying to make sense of your plan, understanding the basic terminology is crucial. In particular, the three most important health insurance terms to grasp are deductibles, premiums, and copays. These terms directly impact how much you’ll pay for coverage and how your insurance works.

In this blog post, we’ll explain these key health insurance terms in simple, easy-to-understand language, explore how they influence your overall healthcare costs, and offer tips on how to choose the best plan based on these factors.

What Is a Health Insurance Premium?

A premium is the amount you pay every month to maintain your health insurance coverage. Whether you use healthcare services that month or not, you still need to pay your premium to keep your policy active.

How Premiums Work

Premiums are paid on a monthly basis, similar to a subscription fee. The amount of your premium can vary significantly depending on your health insurance plan, your age, where you live, and whether you’re getting insurance through your employer, the government, or a private insurer.

Plans with lower premiums might seem more affordable, but they often come with higher deductibles and out-of-pocket costs, which we’ll discuss next. It’s important to strike a balance between affordable monthly premiums and the cost of care when selecting a plan.

What Is a Deductible?

A deductible is the amount of money you need to pay out of pocket for medical services before your health insurance begins to pay. Once you’ve met your deductible, your insurance will start covering a portion of your healthcare costs, according to your plan’s terms.

How Deductibles Work

Let’s say your health insurance plan has a $2,000 deductible. This means you’ll need to pay for the first $2,000 of your medical expenses in a given year before your insurance kicks in. Once you reach this deductible, your insurance will cover a percentage of your costs, often called coinsurance, until you hit your out-of-pocket maximum.

Health insurance plans with lower premiums often have higher deductibles, meaning you’ll pay more before your coverage begins. On the flip side, plans with higher premiums tend to have lower deductibles, making them a better option if you expect to need a lot of medical care.

Types of Deductibles

- Individual Deductible: This applies to one person on a plan. Once this individual meets the deductible, insurance begins covering their services.

- Family Deductible: This is a combined deductible for all family members on the plan. Once the total amount paid by the family reaches the deductible limit, the plan’s coverage starts for everyone.

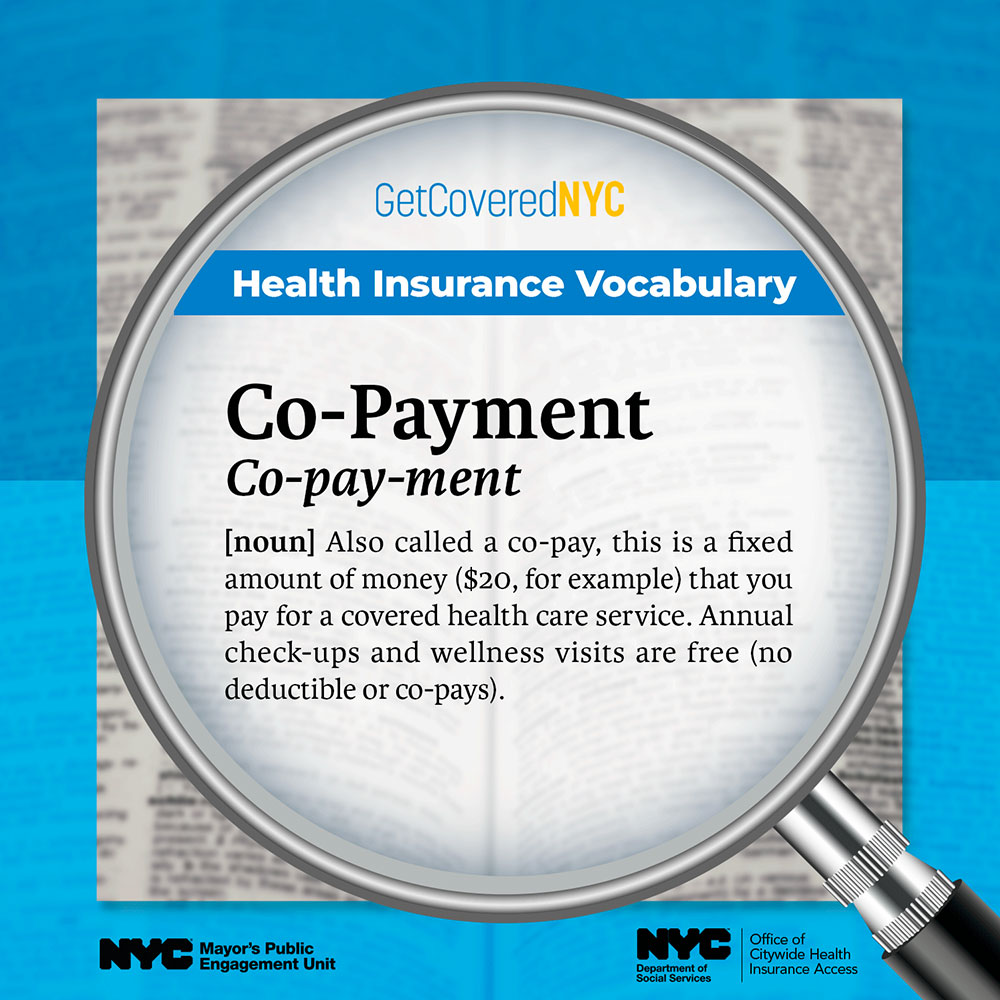

What Is a Copay?

A copay, or copayment, is a fixed amount you pay for a specific healthcare service, such as a doctor’s visit, prescription medication, or a specialist appointment. This amount is usually due at the time of the visit and is a way for you to share the cost of care with your insurance company.

How Copays Work

The copay amount depends on the type of service you’re receiving and your insurance plan. For example, you may have a $25 copay for a primary care doctor visit, but a $50 copay for a specialist or an urgent care visit. Copays are typically lower for routine or preventive services and higher for more specialized care.

It’s important to note that copays often do not count toward your deductible. Even if you haven’t met your deductible for the year, you’ll still pay the set copay amount for specific services. Copays also don’t usually count toward your out-of-pocket maximum.

Understanding Coinsurance

In addition to deductibles and copays, many health insurance plans also include coinsurance. Coinsurance is the percentage of a medical bill you must pay after meeting your deductible.

For example, if your plan has a 20% coinsurance rate, and you’ve already met your deductible, you would be responsible for 20% of the cost of covered services, and your insurance would cover the remaining 80%. Coinsurance rates vary by plan and can significantly impact how much you pay for care.

What Is an Out-of-Pocket Maximum?

An out-of-pocket maximum is the most you’ll have to pay for covered medical expenses in a given year. Once you’ve reached this limit through deductibles, copays, and coinsurance, your insurance will cover 100% of your medical costs for the rest of the year.

The out-of-pocket maximum is a safeguard to prevent you from facing unlimited medical bills in a single year. It’s especially important for those with chronic conditions or who expect to need expensive treatments, as it caps your total spending.

How Do These Terms Affect Your Health Insurance Costs?

Each of these terms—premiums, deductibles, and copays—affects your overall healthcare costs in different ways. Here’s how:

- Premiums: You pay this every month, whether you use healthcare services or not. Higher premiums usually mean better coverage and lower deductibles.

- Deductibles: You need to pay this amount out of pocket before your insurance starts covering your medical expenses. Higher deductibles usually come with lower premiums, but they can mean higher costs if you need a lot of care.

- Copays: These are fixed amounts you pay at the time of service. While copays can add up, they offer a predictable way to share the cost of healthcare services.

Tips for Choosing the Right Health Insurance Plan

Choosing the right health insurance plan involves finding the right balance between premiums, deductibles, copays, and coinsurance. Here are a few tips to help you make an informed decision:

1. Consider Your Healthcare Needs

If you’re generally healthy and don’t expect to need much medical care, you may benefit from a plan with lower premiums and a higher deductible. On the other hand, if you have a chronic condition or expect to need frequent doctor visits or prescriptions, a plan with higher premiums but lower deductibles and copays may be more cost-effective.

2. Look at Total Costs, Not Just Premiums

When comparing health insurance plans, it’s important to consider all costs, not just the monthly premium. A low-premium plan might seem affordable at first, but if it comes with a high deductible and high copays, it could cost you more in the long run if you need medical care.

3. Check the Provider Network

Make sure your preferred doctors and healthcare providers are in the plan’s network. Out-of-network care is often significantly more expensive, and some plans won’t cover out-of-network services at all.

4. Think About Prescription Coverage

If you take prescription medications regularly, make sure your plan covers them at an affordable cost. Check the copays for medications and whether there’s a separate prescription deductible.

Conclusion: Understanding Health Insurance Terms for Better Financial Planning

Understanding key health insurance terms like premiums, deductibles, and copays is essential for choosing the right plan and managing your healthcare expenses. Each of these terms affects how much you’ll pay for medical care and how your insurance works when you need it.

By familiarizing yourself with these concepts and comparing plans based on your healthcare needs and budget, you can make an informed decision that helps you avoid unnecessary costs while ensuring you get the care you need.